Blank Texas 12 302 PDF Template

Form Example

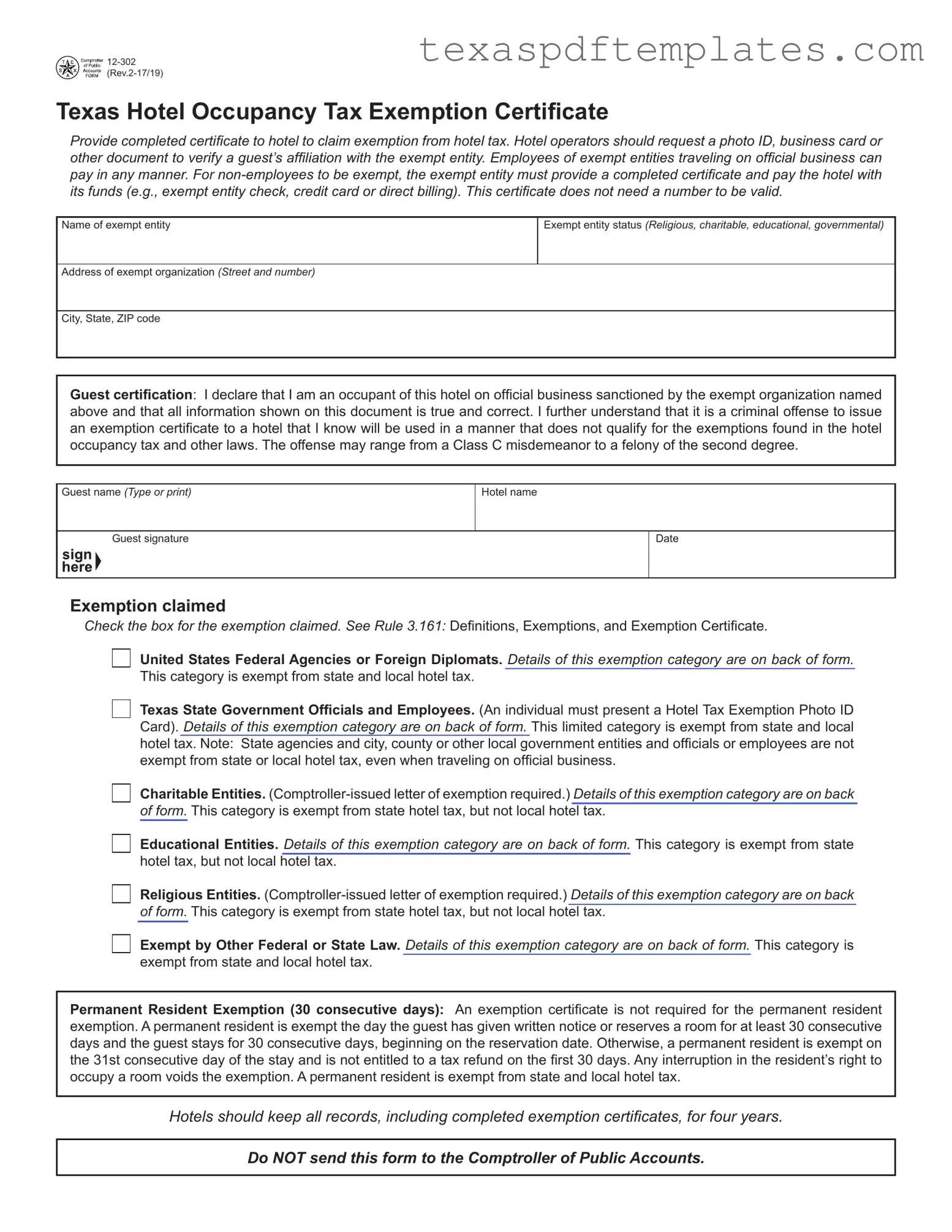

Texas Hotel Occupancy Tax Exemption Certiicate

Provide completed certiicate to hotel to claim exemption from hotel tax. Hotel operators should request a photo ID, business card or other document to verify a guest’s afiliation with the exempt entity. Employees of exempt entities traveling on oficial business can pay in any manner. For

Name of exempt entity

Exempt entity status (Religious, charitable, educational, governmental)

Address of exempt organization (Street and number)

City, State, ZIP code

Guest certiication: I declare that I am an occupant of this hotel on oficial business sanctioned by the exempt organization named above and that all information shown on this document is true and correct. I further understand that it is a criminal offense to issue an exemption certiicate to a hotel that I know will be used in a manner that does not qualify for the exemptions found in the hotel occupancy tax and other laws. The offense may range from a Class C misdemeanor to a felony of the second degree.

Guest name (Type or print)

Hotel name

Guest signature

Date

Exemption claimed

Check the box for the exemption claimed. See Rule 3.161: Deinitions, Exemptions, and Exemption Certiicate.

United States Federal Agencies or Foreign Diplomats. Details of this exemption category are on back of form. This category is exempt from state and local hotel tax.

Texas State Government Oficials and Employees. (An individual must present a Hotel Tax Exemption Photo ID Card). Details of this exemption category are on back of form. This limited category is exempt from state and local hotel tax. Note: State agencies and city, county or other local government entities and oficials or employees are not exempt from state or local hotel tax, even when traveling on oficial business.

Charitable Entities.

Educational Entities. Details of this exemption category are on back of form. This category is exempt from state hotel tax, but not local hotel tax.

Religious Entities.

Exempt by Other Federal or State Law. Details of this exemption category are on back of form. This category is exempt from state and local hotel tax.

Permanent Resident Exemption (30 consecutive days): An exemption certiicate is not required for the permanent resident exemption. A permanent resident is exempt the day the guest has given written notice or reserves a room for at least 30 consecutive days and the guest stays for 30 consecutive days, beginning on the reservation date. Otherwise, a permanent resident is exempt on the 31st consecutive day of the stay and is not entitled to a tax refund on the irst 30 days. Any interruption in the resident’s right to occupy a room voids the exemption. A permanent resident is exempt from state and local hotel tax.

Hotels should keep all records, including completed exemption certiicates, for four years.

Do NOT send this form to the Comptroller of Public Accounts.

Form

Texas Hotel Occupancy Tax Exemptions

See Rule 3.161: Deinitions, Exemptions, and Exemption Certiicate for additional information.

United States Federal Agencies or Foreign Diplomats (exempt from state and local hotel tax)

This exemption category includes the following:

•the United States federal government, its agencies and departments, including branches of the military, federal credit unions, and their employees traveling on oficial business;

•rooms paid by vouchers issued by the American Red Cross and the Federal Emergency Management Agency; and

•foreign diplomats who present a Tax Exemption Card issued by the U.S. Department of State, unless the card speciically excludes hotel occupancy tax.

Federal government contractors are not exempt.

Texas State Government Oficials and Employees (exempt from state and local hotel tax)

This exemption category includes only Texas state oficials or employees who present a Hotel Tax Exemption Photo Identiication Card. State employees without a Hotel Tax Exemption Photo Identiication Card and Texas state agencies are not exempt. (The state employee must pay hotel tax, but their state agency can apply for a refund.)

Charitable Entities (exempt from state hotel tax, but not local hotel tax)

This exemption category includes entities that have been issued a letter of tax exemption as a charitable organization and their employees traveling on oficial business. See website referenced below.

A charitable entity devotes all or substantially all of its activities to the alleviation of poverty, disease, pain and suffering by providing food, clothing, medicine, medical treatment, shelter or psychological counseling directly to indigent or similarly deserving members of society.

Not all 501(c)(3) or nonproit organizations qualify under this category.

Educational Entities (exempt from state hotel tax, but not local hotel tax)

This exemption category includes

A letter of tax exemption from the Comptroller of Public Accounts as an educational organization is not required, but an educational organization might have one.

Religious Organizations (exempt from state hotel tax, but not local hotel tax)

This exemption category includes nonproit churches and their guiding or governing bodies that have been issued a letter of tax exemption from the Comptroller of Public Accounts as a religious organization and their employees traveling on oficial business. See website referenced below.

Exempt by Other Federal or State Law (exempt from state and local hotel tax)

This exemption category includes the following:

•entities exempted by other federal law, such as federal land banks and federal land credit associations and their employees traveling on oficial business; and

•Texas entities exempted by other state law that have been issued a letter of tax exemption from the Comptroller of Public Accounts and their employees traveling on oficial business. See website referenced below. These entities include the following:

•nonproit electric and telephone cooperatives,

•housing authorities,

•housing inance corporations,

•public facility corporations,

•health facilities development corporations,

•cultural education facilities inance corporations, and

•major sporting event local organizing committees.

For Exemption Information

A list of charitable, educational, religious and other organizations that have been issued a letter of exemption is online at www.comptroller.texas.gov/taxes/exempt/search.php. Other information about Texas tax exemptions, including applications, is online at www.comptroller.texas.gov/taxes/exempt/index.php. For questions about exemptions, call

More PDF Templates

Motion to Enforce Visitation Texas - The Capias is an official document issued upon a judge’s order, pursuing enforcement actions effectively.

Texas Courts - Provisions in the form emphasize the ethical responsibilities of attorneys representing offenders.

Common mistakes

-

Incomplete Information: Failing to fill in all required fields can lead to delays or denials. Each section of the form is important for establishing eligibility for the exemption.

-

Incorrect Entity Status: Selecting the wrong exemption category can invalidate the certificate. Ensure that the status accurately reflects the organization’s classification.

-

Missing Signatures: The guest must sign the form to certify that the information provided is accurate. An unsigned form is not valid.

-

Failure to Check Exemption Claimed: Not marking the appropriate exemption box can lead to confusion and may result in tax charges. Be sure to check the correct exemption category.

-

Inaccurate Guest Certification: Providing false information in the guest certification section can have serious legal consequences. Always ensure the declaration is truthful.

-

Not Providing Supporting Documents: For certain exemptions, such as charitable or religious entities, a letter of exemption may be required. Be prepared to provide this documentation.

-

Ignoring Permanent Resident Rules: Misunderstanding the rules regarding permanent residents can lead to unnecessary tax charges. Remember, a written notice for a stay of 30 consecutive days is essential.

-

Incorrect Payment Method: Non-employees must ensure that the hotel is paid with the exempt entity’s funds. Using personal funds can invalidate the exemption.

-

Failure to Retain Records: Not keeping copies of completed exemption certificates can lead to issues if questioned by tax authorities. Hotels should maintain these records for four years.

Key takeaways

- Purpose of the Form: The Texas 12-302 form is essential for claiming an exemption from hotel occupancy tax. It must be completed and provided to the hotel by the guest.

- Verification Requirement: Hotel operators should request a photo ID or other documents to verify the guest’s affiliation with the exempt entity, ensuring compliance with tax regulations.

- Exemption Categories: There are several exemption categories, including federal agencies, state government officials, charitable entities, educational institutions, and religious organizations. Each category has specific requirements for exemption.

- Permanent Resident Exemption: Guests who stay for 30 consecutive days or more do not need to submit the form. They become exempt from hotel tax on the 31st day of their stay.

- Record Keeping: Hotels are required to keep completed exemption certificates for four years. It is important to note that this form should not be sent to the Comptroller of Public Accounts.

Steps to Using Texas 12 302

Completing the Texas 12-302 form is essential for claiming an exemption from hotel occupancy tax. Once you fill out the form, provide it to the hotel to ensure the exemption is honored. Be sure to gather any necessary documents to support your claim.

- Identify the exempt entity: Write the name of the exempt organization at the top of the form.

- Specify the exempt entity status: Choose the appropriate status from the options provided (e.g., Religious, Charitable, Educational, Governmental).

- Provide the address: Fill in the street address, city, state, and ZIP code of the exempt organization.

- Guest certification: In this section, type or print your name as the guest. Confirm that you are staying on official business and that the information is accurate.

- Sign the form: Add your signature and the date to validate the certification.

- Hotel name: Enter the name of the hotel where you are staying.

- Claim the exemption: Check the box corresponding to the exemption category you are claiming.

Once the form is completed, make sure to provide it to the hotel management. Keep a copy for your records, as it may be needed for future reference or verification. Remember, hotels are required to keep these records for four years, so ensure all information is accurate and complete.